As the housing market continues to change, you may be wondering where it’ll go from here. One factor you’re probably thinking about is home prices, which have come down a bit since they peaked last June. And you’ve likely heard something in the news or on social media about a price crash on the horizon. As a result, you may be holding off on buying a home until prices drop significantly. But that’s not the best strategy.

A recent survey from Zonda shows 53% of millennials are still renting right now because they’re waiting for home prices to come down. But here’s the thing: the most recent data shows that home prices appear to have bottomed out and are now on the rise again. Selma Hepp, Chief Economist at CoreLogic, reports:

“U.S. home prices rose by 0.8% in February . . . indicating that prices in most markets have already bottomed out.”

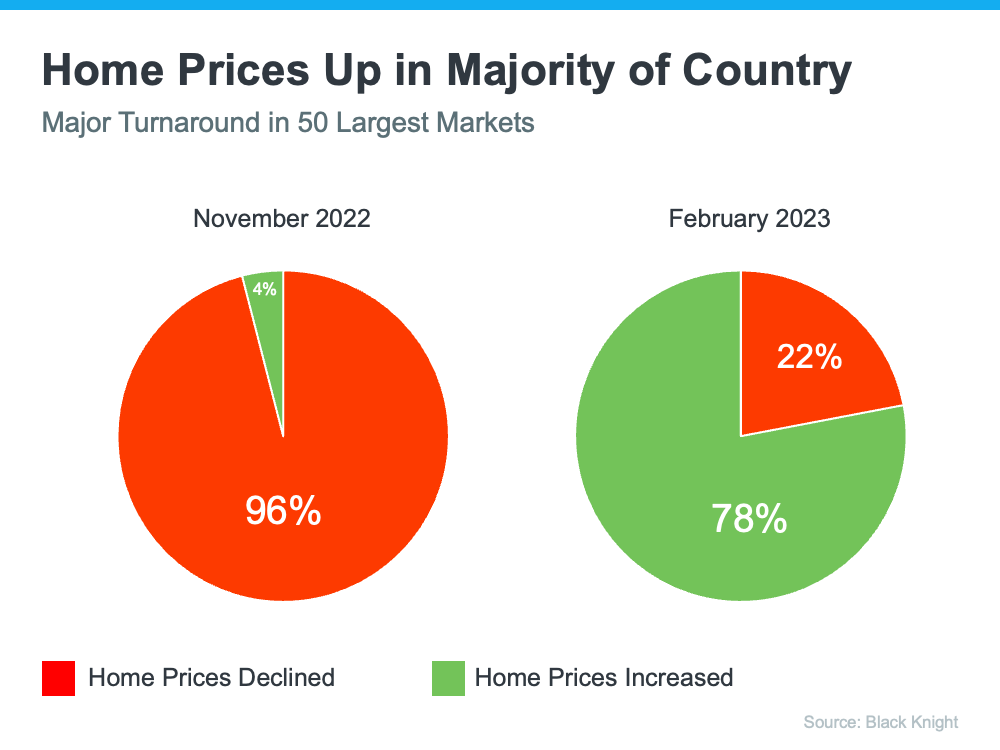

And the latest data from Black Knight shows the same shift. The graph below compares home price trends in November to those in February:

So, should you keep waiting to buy a home until prices come down? If you factor in what the experts are saying, you probably shouldn’t. The data shows prices are increasing in much of the country, not decreasing. And the latest data from the Home Price Expectation Survey indicates that experts project home prices will rise steadily and return to more normal levels of appreciation after 2023. The best way to understand what home values are doing in your area is to work with a local real estate professional who can give you the latest insights and expert advice.

Bottom Line

If you’re waiting to buy a home until prices come down, you may want to reconsider. Let’s connect to make sure you understand what’s happening in our local housing market.

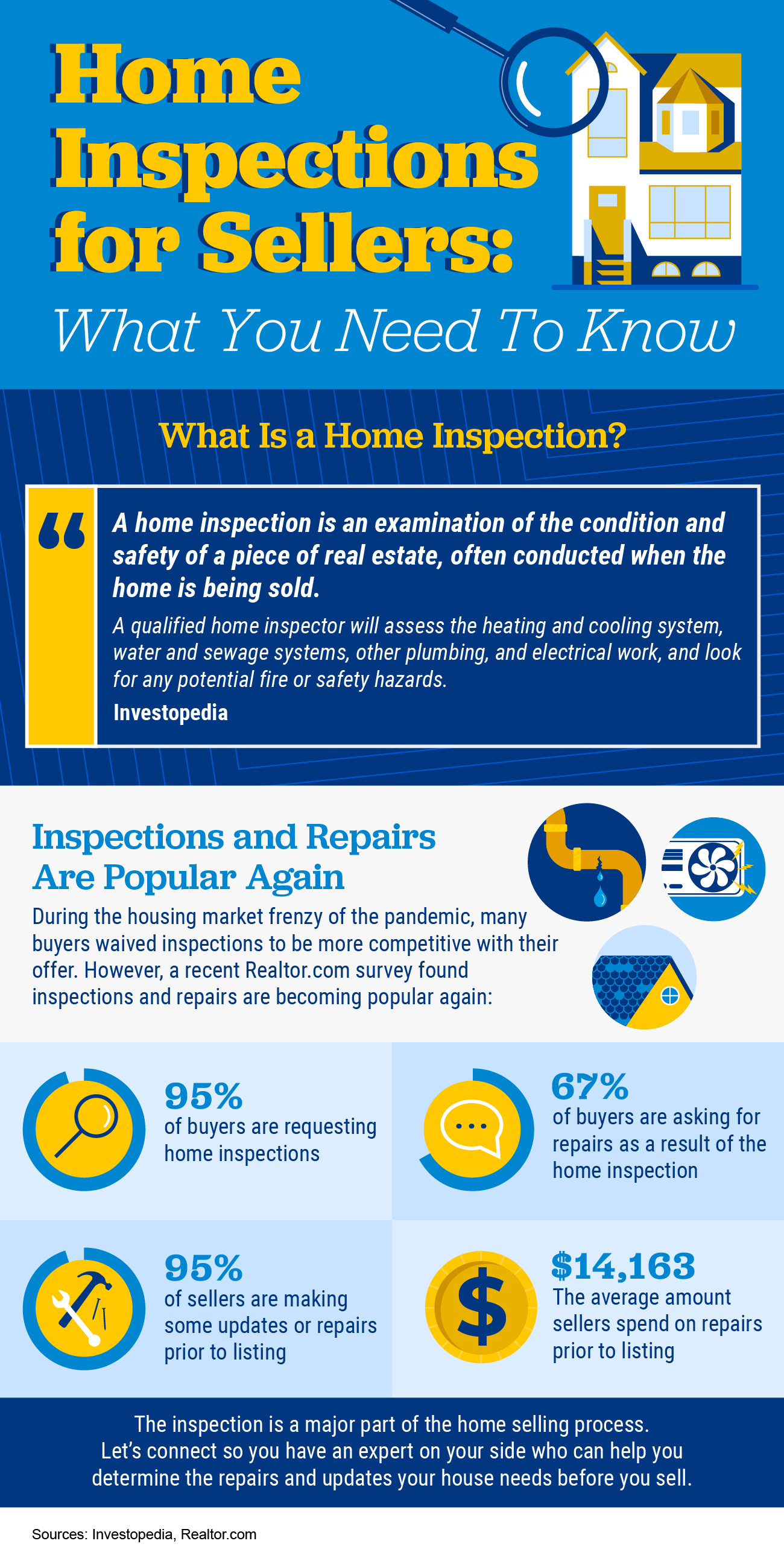

Thinking about selling your house? If you’ve been waiting for the right time, it could be now while the supply of homes for sale is so low. HousingWire shares:

“. . . the big question is whether we are finally starting to see the seasonal spring increase in inventory. The answer is no, because active listings fell to a new low last week for 2023 . . .”

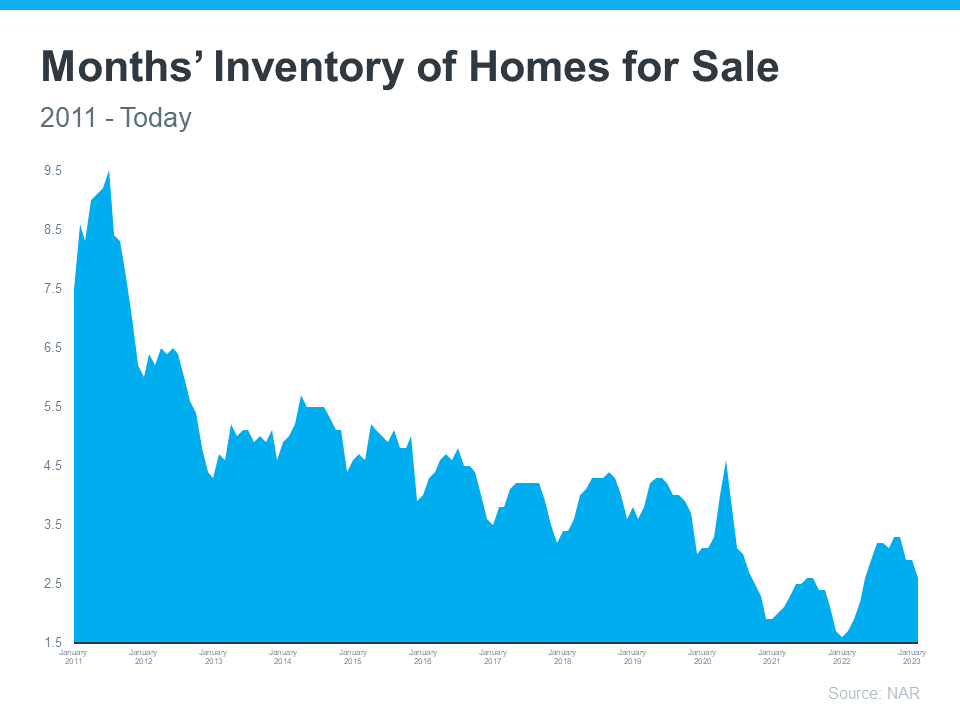

The National Association of Realtors (NAR) confirms today’s housing inventory is low by looking at the months’ supply of homes on the market. In a balanced market, about a six-month supply is needed. Anything lower is a sellers’ market. And today, the number is much lower:

“Total housing inventory registered at the end of February was 980,000 units, identical to January and up 15.3% from one year ago (850,000). Unsold inventory sits at a 2.6-month supply at the current sales pace, down 10.3% from January but up from 1.7 months in February 2022.”

Why Does Low Inventory Make It a Good Time To Sell?

The less inventory there is on the market when you sell, the less competition you’re likely to face from other sellers. That means your house will get more attention from the buyers looking for a home this spring. And since there are significantly more buyers in the market than there are homes for sale, you could even receive more than one offer on your house. Multiple offers are on the rise again (see graph below):

If you get more than one offer on your house, it becomes a bidding war between buyers – and that means you have greater leverage to sell on your terms. But if you want to maximize the opportunity for a bidding war to spark, be sure to lean on your expert real estate advisor. While we’re still in a strong sellers’ market, it isn’t the frenzy we saw a couple of years ago, and today’s buyers are focused on the houses with the greatest appeal. Clare Trapasso, Executive News Editor at Realtor.com, explains:

“Well-priced, move-in ready homes with curb appeal in desirable areas are still receiving multiple offers and selling for over the asking price in many parts of the country. So, this spring, it’s especially important for sellers to make their homes as attractive as possible to appeal to as many buyers as possible.”

Bottom Line

If you’ve been waiting for the right time to sell your house, low inventory this spring sets you up with a big advantage. Let’s connect today to make sure your house is ready to sell.

The spring season appears to be warming up in housing as more and more buyers enter the market. And after rising mortgage rates sidelined so many buyers last year, that’s a good sign for sellers. Realtor.comhas the latest:

“Spring is officially here, and like green shoots emerging from the bleak winter, new data suggests that more buyers are back in the market, although more subdued compared to a year ago.”

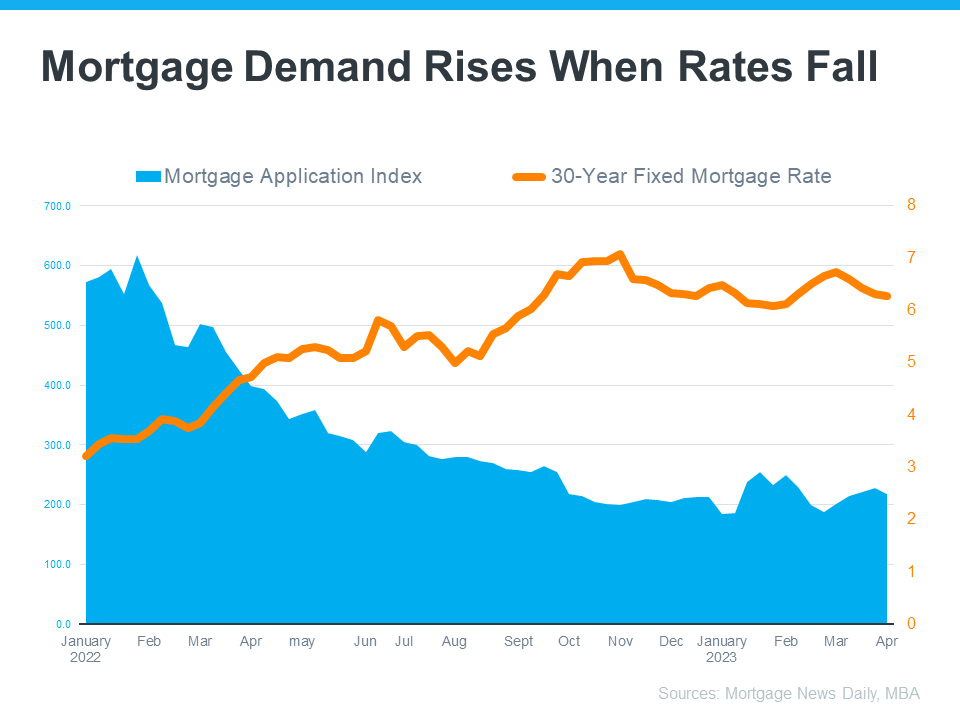

We know buyer activity is trending up because of mortgage purchase application data. According to Investopedia:

“A mortgage application is a document submitted to a lender when you apply for a mortgage to purchase real estate.”

That means the number of mortgage applications shows how many buyers are applying for mortgages. Put another way, an increase in mortgage applications means an increase in buyer demand – and as Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), explains, application activity started ramping up as mortgage rates fell steadily in March:

“Application activity increased as mortgage rates declined . . . recent increases, along with data from other sources showing an uptick in home sales, is a welcome development.”

In fact, we can see how mortgage rates have a direct impact on applications over time. As rates rose dramatically last year, applications fell in response (see graph below):

The recent uptick in mortgage applications, as well as the decline in mortgage rates, is good news for sellers because it means more buyers are actively looking for homes.

What This Means for You

Buyers are coming this spring, which is typically the busiest time of the year in real estate. And as Realtor.comtells us, if you’re a seller, you need to prepare:

“If homeowners are planning to sell in 2023, now is the time to get ready.”

The means working with a local real estate agent to maximize your home’s appeal and get it listed at the ideal price for your area.

Bottom Line

The housing market is warming up for spring. If you’re thinking about selling your house and taking advantage of this recent uptick in buyer activity, let’s connect.

There have been a lot of shifts in the housing market recently. Mortgage rates rose dramatically last year, impacting many people’s ability to buy a home. And after several years of rapid price appreciation, home prices finally peaked last summer. These changes led to a rise in headlines saying prices would end up crashing.

Even though we’re no longer seeing the buyer frenzy that drove home values up during the pandemic, prices have been relatively flat at the national level. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), doesn’t expect that to change:

“[H]ome prices will be steady in most parts of the country with a minor change in the national median home price.”

You might think sellers would have to lower prices to attract buyers in today’s market, and that’s part of why some may have been waiting for prices to come crashing down. But there’s another factor at play – low inventory. And according to Yun, that’s limiting just how low prices will go:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

As you can see in the graph below, we’ve been at or near record-low inventory levels for a few years now.

That lack of available homes on the market is putting upward pressure on prices. Bankrateputs it like this:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equation simply won’t allow a price crash in the near future.”

If more homes don’t come to the market, a lack of supply will keep prices from crashing, and, according to industry expert Rick Sharga, inventory isn’t likely to rise significantly this year:

“I believe that we’re likely to see low inventory continue to vex the housing market throughout 2023.”

Sellers are under no pressure to move since they have plenty of equity right now. That equity acts as a cushion for homeowners, lowering the chances of distressed sales like foreclosures and short sales. And with many homeowners locked into low mortgage rates, that equity cushion isn’t going anywhere soon.

With so few homes available for sale today, it’s important to work with a trusted real estate agent who understands your local area and can navigate the current market volatility.

Bottom Line

A lot of people expected prices would crash this year thanks to low buyer demand, but that isn’t happening. Why? There aren’t enough homes for sale. If you’re thinking about moving this spring, let’s connect.

Wondering if you should sell your house this year? As you make your decision, think about what’s motivating you to consider moving. A recent survey from realtor.com asked why homeowners are thinking about selling their houses this year. Here are the top two reasons (see graphic below):

Let’s break those reasons down and explore how they might resonate with you.

1. I Want To Take Advantage of the Current Market and Make a Profit

When you decide to sell your house, how much you’ll make from the sale will likely be top of mind. So, here’s some good news: according to the latest data, the average seller can expect a strong return on their investment when they make a move. ATTOM explains:

“The $112,000 profit on median-priced home sales in 2022 represented a 51.4% return on investment compared to the original purchase price, up from 44.6% last year and from 32.8% in 2020.”

Even though home prices have declined slightly in some markets, they’re still much higher overall than they were just a few years ago. To understand what’s happening with home prices in your area and the current value of your house, work with a local real estate professional. They can give you the best advice on how much you could gain if you sell this year.

2. My Home No Longer Meets My Needs

The average person has been in their house for ten years. That’s a long time when you think about how much may have changed in your life since you moved in. And typically, those changes have a direct impact on what you need in a home. Whether it’s more (or less) space, different features, or a location closer to your work or loved ones, your current house may no longer check all the boxes of what feels like home to you. If that’s the case, it could be time to work with a real estate agent to find a better fit.

Bottom Line

If you’re thinking about selling your house, there’s probably a good reason for it. Let’s connect so you can make a move that’ll help you accomplish your goals this year.

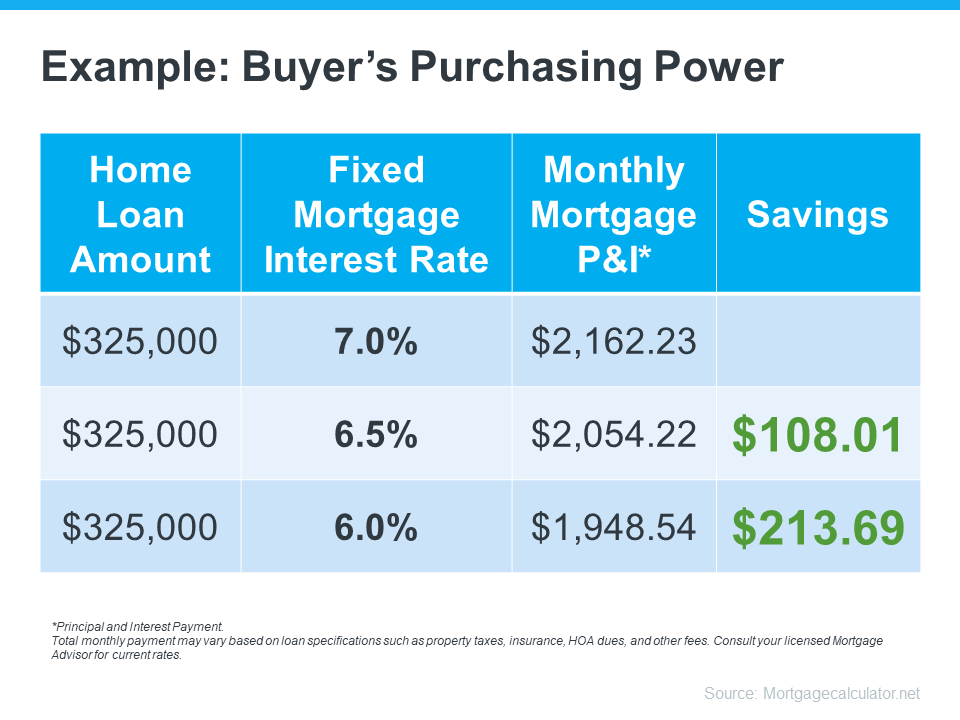

The 30-year fixed mortgage rate has been bouncing between 6% and 7% this year. If you’ve been on the fence about whether to buy a home or not, it’s helpful to know exactly how a 1%, or even a 0.5%, mortgage rate shift affects your purchasing power.

The chart below helps show the general relationship between mortgage rates and a typical monthly mortgage payment:

Even a 0.5% change can have a big impact on your monthly payment. And since rates have been moving between 6% and 7% for a while now, you can see how it impacts your purchasing power as rates go down.

What This Means for You

You may be tempted to put your homebuying plans on hold in hopes that rates will fall. But that can be risky. No one knows for sure where rates will go from here, and trying to time them for your benefit is tough. Lisa Sturtevant, Housing Economist at Bright MLS, explains:

“It is typically a fool’s errand for a homebuyer to try to time rates in this market . . . But volatility in mortgage rates right now can have a real impact on buyers’ monthly payments.”

That’s why it’s critical to lean on your expert real estate advisors to explore your mortgage options, understand what impacts mortgage rates, and plan your homebuying budget around today’s volatility. They’ll also be able to offer advice tailored to your specific situation and goals, so you have what you need to make an informed decision.

Bottom Line

Your ability to buy a home could be impacted by changing mortgage rates. If you’re thinking about making a move, let’s connect so you have a strong plan in place.

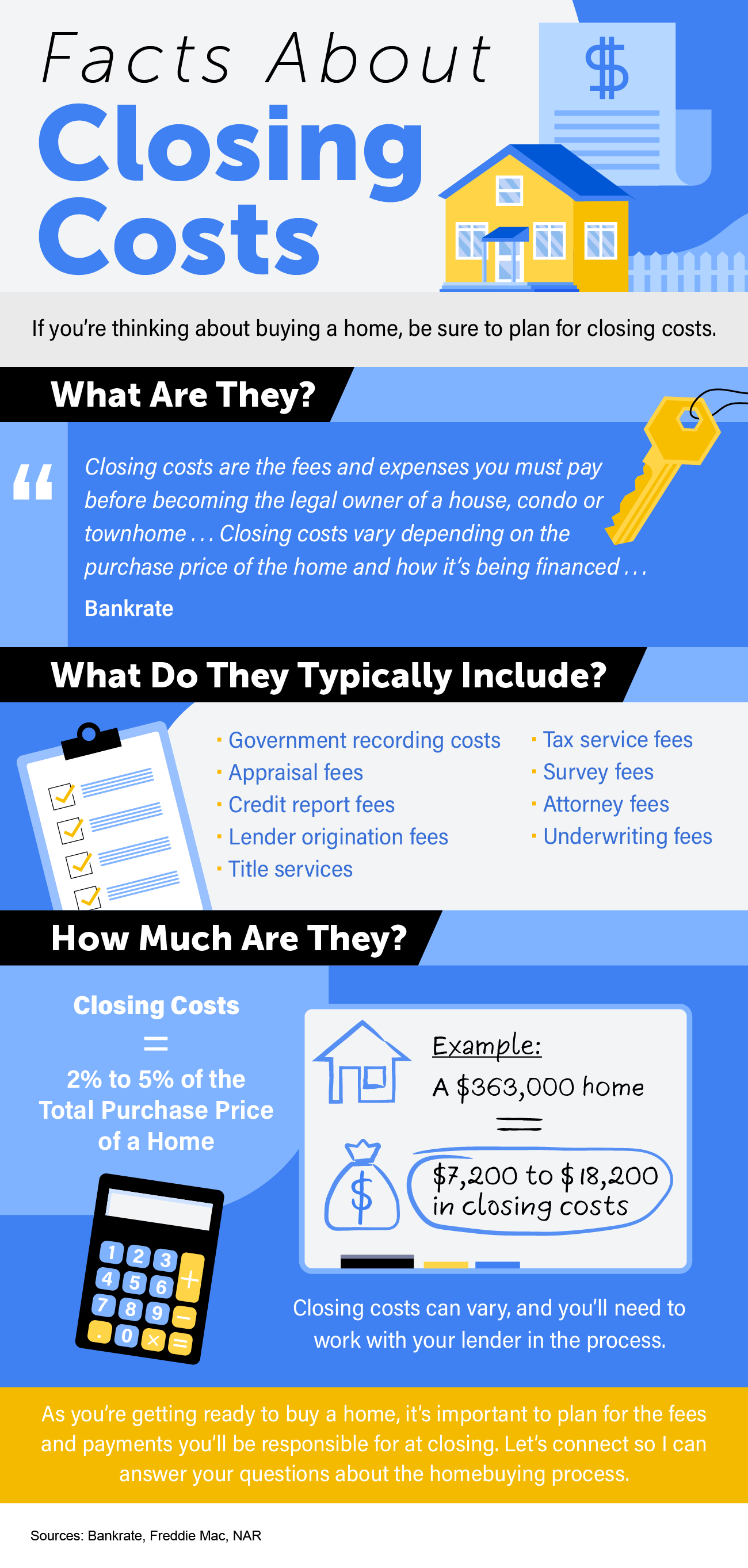

Closing costs are typically 2% to 5% of the total purchase price of a home, and they can include things like government recording costs, appraisal fees, and more.

Let’s connect so I can answer your questions about the homebuying process.

Spring has arrived, and that means more and more people are getting their homes ready to sell. But with recent shifts in real estate, this year’s spring housing market will be different from the frenzy of the past several years. To sell your house quickly, without hassles, and for the most money, be sure to follow these four simple tips:

1. Make Sure You Give Buyers Access

One of the biggest mistakes you can make as a seller is limiting the days and times when buyers have access to view your home. In any market, if you want to maximize the sale of your house, you can’t limit potential buyers’ access to view it. If it’s not accessible, it could cost you by sitting on the market longer and ultimately selling for a lower price.

2. Make Your Home Look as Good as Possible on the Inside

For anything to sell, especially your home, it must look inviting. Your real estate agent can give you expert advice on ideal staging for your home. Even updating a room with fresh paint, steam cleaning carpets, or removing clutter from the garage can make a big impact.

3. First Impressions Matter

The old saying “you never get a second chance to make a first impression” matters when selling your house. Often, the first impression a buyer gets is what they see as they walk up to the front door. Putting in the work in on the exterior of your home is just as important as what you stage inside. Freshen up your landscaping to improve your home’s curb appeal so you can make an impact with potential buyers.

4. Price It Right

This is probably the most important aspect of selling your home in today’s real estate market. If a house is priced competitively, it’s going to sell. Period. To do this, you have to know what’s happening with home prices in your area and understand the factors that are affecting the market right now. That’s why it’s best to work with a trusted real estate professional who can ensure you list your house at the right price.

Bottom Line

Everyone selling their home wants three things: to sell it for the most money they can, to do it in a certain amount of time, and to do all of that with the fewest hassles. To accomplish these goals, let’s connect so you can understand the steps you need to take to sell your home this spring.

It doesn’t matter if you’re someone who closely follows the economy or not, chances are you’ve heard whispers of an upcoming recession. Economic conditions are determined by a broad range of factors, so rather than explaining them each in depth, let’s lean on the experts and what history tells us to see what could lie ahead. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Two-in-three economists are forecasting a recession in 2023 . . .”

As talk about a potential recession grows, you may be wondering what a recession could mean for the housing market. Here’s a look at the historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession could mean for the housing market today.

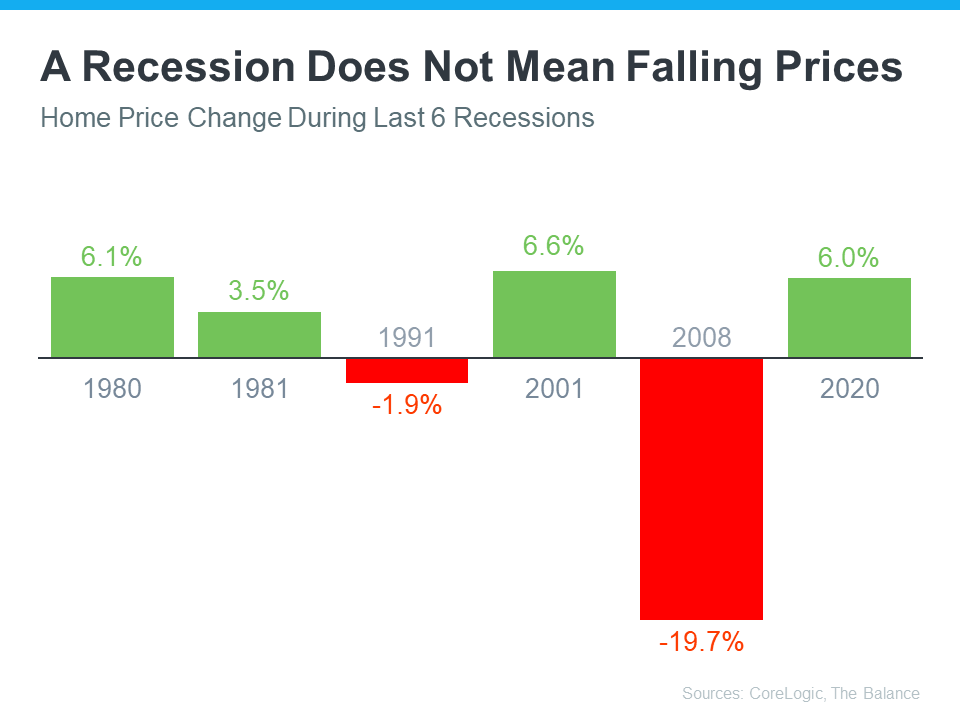

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at recessions going all the way back to 1980, home prices appreciated in four of the last six of them. So historically, when the economy slows down, it doesn’t mean home values will always fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would be a repeat of what happened to housing then. But today’s housing market isn’t about to crash because the fundamentals of the market are different than they were in 2008. According to experts, home prices will vary by market and may go up or down depending on the local area. But the average of their 2023 forecasts shows prices will net neutral nationwide, not fall drastically like they did in 2008.

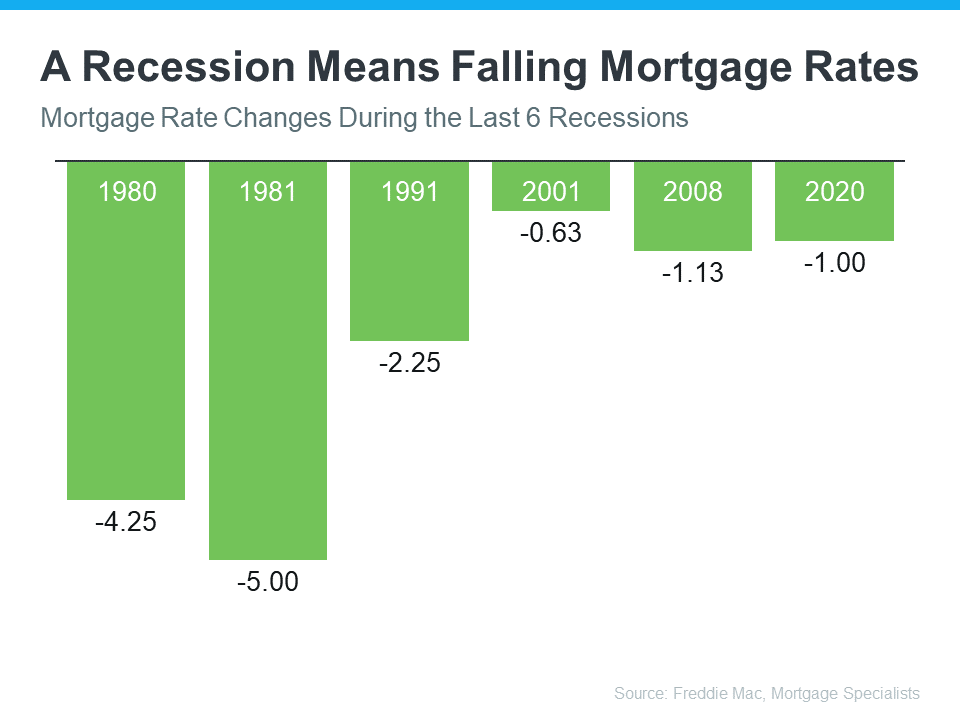

A Recession Means Falling Mortgage Rates

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the graph below shows, historically, each time the economy slowed down, mortgage rates decreased.

Fortuneexplains mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

In 2023, market experts say mortgage rates will likely stabilize below the peak we saw last year. That’s because mortgage rates tend to respond to inflation. And early signs show inflation is starting to cool. If inflation continues to ease, rates may fall a bit more, but the days of 3% are likely behind us.

The big takeaway is you don’t need to fear the word recession when it comes to housing. In fact, experts say a recession would be mild and housing would play a key role in a quick economic rebound. As the 2022 CEO Outlook from KPMG, says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . .

More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

Bottom Line

While history doesn’t always repeat itself, we can learn from the past. According to historical data, in most recessions, home values have appreciated and mortgage rates have declined.

If you’re thinking about buying or selling a home this year, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link