Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Mid-Year Market Update for 2024: What Buyers and Sellers Need to Know

Last December, when the Federal Reserve projected a series of benchmark rate cuts in the coming year, some analysts speculated that mortgage rates—which had recently peaked near 8%—would fall closer to 6% by mid-2024.1,2,3 Unfortunately, persistent inflation has delayed the central bank’s timeline and kept the average 30-year mortgage rate hovering around 7% so far this year.2

While elevated mortgage rates have continued to dampen the pace of home sales and affordability, there have been some positive developments for frustrated homebuyers. Nationwide, the inventory shortage is starting to ease, and an uptick in starter homes coming on the market has helped to slow the median home price growth rate, presenting some relief to cash-strapped buyers.4

There are also signs that sellers are adjusting to the higher rate environment, as a growing number list their properties for sale.4 Still, economists say a persistent housing deficit—combined with tighter lending standards and historically high levels of home equity—will help keep the market stable.5

What does that mean for you? Read on for our take on this year’s most important real estate news and get a sneak peek into what analysts predict is around the corner for 2024.

MORTGAGE RATE CUTS WILL TAKE LONGER THAN EXPECTED

At its most recent meeting on May 1, the Federal Reserve announced that it would keep its overnight rate at a 23-year high in response to the latest, still-elevated inflation numbers.6

While mortgage rates aren’t directly tied to the federal funds rate, they do tend to move in tandem. So, while expected, the Fed’s announcement was further proof that a meaningful decline in mortgage rates—and a subsequent real estate market rebound—is farther off than many experts predicted.

“The housing market has always been interest rate sensitive. When rates go up, we tend to see less activity,” explained Realtor.com chief economist Danielle Hale in a recent article. “The housing market is even more rate sensitive now because many people are locked into low mortgage rates and because first-time buyers are really stretched by high prices and borrowing costs.”7

Many experts now speculate that the first benchmark rate cut will come no sooner than September, so homebuyers hoping for a cheaper mortgage will have to remain patient.

“We’re not likely to see mortgage rates decline significantly until after the Fed makes its first cut; and the longer it takes for that to happen, the less likely it is that we’ll see rates much below 6.5% by the end of the year,” predicted Rick Sharga, CEO at CJ Patrick Company, in a May interview.8What does it mean for you? Mortgage rates aren’t expected to fall significantly any time soon, but that doesn’t necessarily mean you should wait to buy a home. A drop in rates could lead to a spike in home prices if pent-up demand sends a flood of homebuyers back into the market. Reach out to schedule a free consultation so we can help you chart the best course for your home purchase or sale.

BUYERS ARE GAINING OPTIONS AS SELLERS RETURN TO THE MARKET

There is a silver lining for buyers who have struggled to find the right property: More Americans are sticking a for-sale in their yard.9 Given the record-low inventory levels of the past few years, this presents an opportunity for buyers to find a place they love—and potentially score a better deal.

In 2023, inventory remained scarce as homeowners who felt beholden to their existing mortgage rates delayed their plans to sell. However, a recent survey by Realtor.com shows that a growing number of those owners are ready to jump in off the sidelines.10

While the majority of potential sellers still report feeling “locked in” by their current mortgage, the share has declined slightly (79% now versus 82% in 2023). Additionally, nearly one-third of those “locked-in” owners say they need to sell soon for personal reasons, and the vast majority (86%) report that they’ve already been thinking about selling for more than a year.10

Renewed optimism may also be playing a part. “Both our ‘good time to buy’ and ‘good time to sell’ measures continued their slow upward drift this month,” noted Fannie Mae Chief Economist Doug Duncan in an April statement.11

However, the current stock of available homes still falls short of pre-pandemic levels, according to economists at Realtor.com. “For the first four months of this year, the inventory of homes actively for sale was at its highest level since 2020. However, while inventory this April is much improved compared with the previous three years, it is still down 35.9% compared with typical 2017 to 2019 levels.”4\

What does it mean for you? If you’ve had trouble finding a home in the past, you may want to take another look. An increase in inventory, coupled with relatively low buyer competition, could make this an ideal time to make a move. Reach out if you’re ready to search for your next home.

If you’re hoping to sell this year, you may also want to act now. If inventory levels grow, it will become more challenging for your home to stand out. We can craft a plan to maximize your profits, starting with a professional assessment of your home’s current market value. Contact us to schedule a free consultation.

HOME PRICES ARE RISING AT A MORE MANAGEABLE PACE

Homebuyers struggling with high borrowing costs have something else to celebrate. The national median home price has remained relatively stable over the past year, due to sellers bringing a greater share of smaller, more affordable homes to the market.4

In addition to offering cheaper homes, a recent survey found that home sellers are also adjusting their expectations when it comes to pricing. In many regions, just 12% anticipate a bidding war (down from 23% last year) and only 15% expect to sell above list price (versus 31% in 2023).10

But buyers shouldn’t expect a fire sale. According to Realtor.com’s April Housing Market Trends Report, “On an adjusted per-square-foot basis, the median list price grew by 3.8%, as homes continue to retain their value despite increased inventory compared with last year.”4

Dr. Selma Hepp, chief economist for the data firm CoreLogic, projects that home prices will keep rising at a gradual pace through the rest of 2024. “Spring home price gains are already off to a strong start despite continued mortgage rate volatility. That said, more inventory finally coming to market will likely translate to more options for buyers and fewer bidding wars, which typically keeps outsized price growth in check.”12

What does it mean for you? An increase in more affordable housing stock is great news, especially for first-time buyers. And with home values expected to keep rising, an investment in real estate could help you build wealth over time. Reach out to discuss your goals and budget, and we can help you decide if you’re ready to take your first step on the property ladder.

DESIRE TO OWN PERSISTS, BUT AFFORDABILITY REMAINS AN OBSTACLE

Surveys show that the American dream of homeownership is alive and well, despite the financial challenges. In fact, a recent poll by Realtor.com found that 55% of Millennial and 40% of Gen Z respondents believe that now is a good time to buy a home.13

According to Fannie Mae Chief Economist Doug Duncan, buyers are starting to adapt to the new economic reality. “With the historically low rates of the pandemic era now firmly behind us, some households appear to be moving past the hurdle of last year’s sharp jump in rates, an adjustment that we think could help further thaw the housing market. We noted in our latest monthly forecast that we expect to see a gradual increase in home listings and sales transactions in the coming year.”

The Realtor.com study also revealed that even a small drop in mortgage rates could give a big boost to homebuyer demand and affordability. In fact, 40% of the buyers polled would find a home purchase attainable if rates fall under 6%, and an additional 32% plan to enter the market if rates dip below 5%.13

But waiting for rates to drop isn’t the only approach that Americans are using to afford a home. A survey by U.S. News & World Report found that determined homebuyers are employing a variety of strategies, including shopping multiple lenders (52%), purchasing discount points to lower their rates (36%), and opting for adjustable-rate mortgages (36%). More than three-quarters of today’s buyers also hope to refinance to a lower rate in the future.14

Despite the obstacles, these respondents remain steadfast in their desire to own a home, listing financial benefits, stability, and more space as their top motivations for wanting to buy.14

What does it mean for you? If you’re dreaming of a new home, let’s talk. We can help you evaluate your options and connect you with a mortgage professional to discuss strategies you can use to make your monthly payments more affordable. And remember, in many cases, you can refinance if rates drop in the future.

If you have plans to sell, it will be crucial to enlist the help of a skilled agent who knows how to maximize your profit margins and draw in qualified buyers. Reach out for a copy of our multi-step Property Marketing Plan.

I AM HERE TO GUIDE YOU

While national housing reports can give you a “big picture” outlook, much of real estate is local. And as a local market expert, I know what’s most likely to impact sales and drive home values in your particular neighborhood. As a trusted partner in your real estate journey, I can guide you through the market’s twists and turns.

If you’re considering buying or selling a home in 2024, contact us now to schedule a free consultation. Let’s work together and craft an action plan to meet your real estate goals.

The above references an opinion and is for informational purposes only. It is not intended to be financial, legal, or tax advice. Consult the appropriate for advice regarding your individual needs.

Sources:

- CBS News – https://www.cbsnews.com/news/federal-reserve-rate-decision-pause-december-13/

- Bankrate – https://www.bankrate.com/mortgages/historical-mortgage-rates/

- Fannie Mae – https://www.fanniemae.com/media/50096/display

- Realtor.com – https://www.realtor.com/research/april-2024-data/

- Bankrate – https://www.bankrate.com/real-estate/is-the-housing-market-about-to-crash/

- NPR – https://www.npr.org/2024/05/01/1248454950/federal-reserve-inflation-interest-rates

- Realtor.com – https://www.realtor.com/news/trends/will-the-fed-cut-interest-rates-2024-housing-market/

- The Mortgage Reports – https://themortgagereports.com/32667/mortgage-rates-forecast-fha-va-usda-conventional

- Fast Company – https://www.fastcompany.com/91106568/housing-market-inventory-rising-across-country-maps

- Realtor.com – https://www.realtor.com/research/2023-q1-sellers-survey-btts/

- Fannie Mae – https://www.fanniemae.com/research-and-insights/surveys-indices/national-housing-survey

- CoreLogic – https://www.corelogic.com/press-releases/corelogic-us-annual-home-price-growth-slows-still-up-by-over-5-february/

- Realtor.com – https://www.realtor.com/research/america-dream-survey-feb-2024/

- US News & World Report – https://money.usnews.com/loans/mortgages/articles/2024-homebuyer-survey

East Texas: What’s Really Happening with Mortgage Rates?

Mortgage rates don’t move in a straight line. There are too many factors at play for that to happen. Instead, rates bounce around because they’re impacted by things like economic conditions, decisions from the Federal Reserve, and so much more. That means they might be up one day and down the next depending on what’s going on in the economy and the world as a whole.

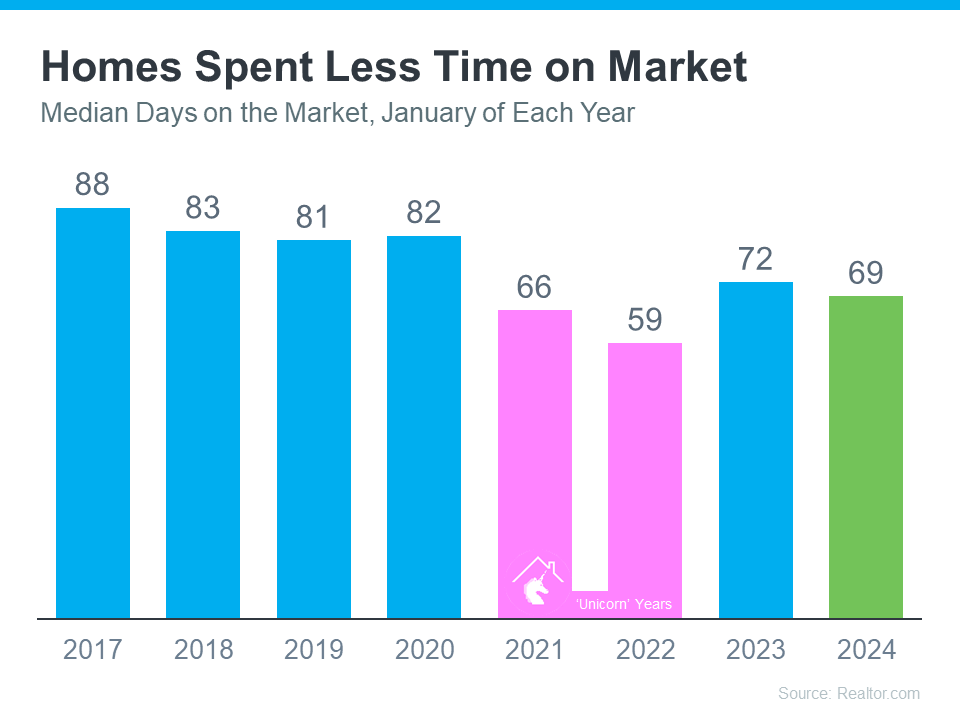

Houses Are Still Selling Fast

Have you been thinking about selling your house? If so, here’s some good news. While the housing market isn’t as frenzied as it was during the ‘unicorn’ years when houses were selling quicker than ever, they’re still selling faster than normal.

The graph below uses data from Realtor.com to tell the story of median days on the market for every January from 2017 all the way through the latest numbers available. For Realtor.com, days on the market means from the time a house is listed for sale until its closing date or the date it’s taken off the market. This metric can help give you an idea of just how quickly homes are selling compared to more normal years:

When you look at the most recent data (shown in green), it’s clear homes are selling faster than they usually would (shown in blue). In fact, the only years when houses sold even faster than they are right now were the abnormal ‘unicorn’ years (shown in pink). According to Realtor.com:

“Homes spent 69 days on the market, which is three days shorter than last year and more than two weeks shorter than before the COVID-19 pandemic.”

What Does This Mean for You?

Homes are selling faster than the norm for this time of year – and your house may sell quickly too. That’s because more people are looking to buy now that mortgage rates have come down, but there still aren’t enough homes to go around. Mike Simonsen, Founder of Altos Research, says:

“. . . 2024 is starting stronger than last year. And demand is increasing each week.”

Bottom Line

If you’re wondering if it’s a good time to sell your home, the most recent data suggests it is. The housing market appears to be stronger than it usually is at this time of year. To get the latest updates on what’s happening in our local market, let’s connect.

Are More Homes Coming onto the Market?

Are More Homes Coming onto the Market?

The number of homes for sale is an essential factor shaping today’s market. And, if you’re considering whether or not to list your house, that’s one of the biggest advantages you have right now. When housing inventory is this low, your house will stand out, especially if it’s priced right.

But there are some early signs that more listings are coming. According to the latest data, new listings (homeowners who just put their house up for sale) are trending up. Here’s a look at why this is noteworthy and what it may mean for you.

More Homes Are Coming onto the Market than Usual

It’s well known that the busiest time in the housing market each year is the spring buying season. That’s why there’s a predictable increase in the volume of newly listed homes throughout the first half of the year. Sellers are anticipating this and ramping up for the months when buyers are most active. But, as the school year kicks off and as the holidays approach, the market cools. It’s what’s expected.

But here’s what’s surprising. Based on the latest data from Realtor.com, there’s an increase in the number of sellers listing their houses later this year than usual. A peak this late in the year isn’t typical. You can see both the normal seasonal trend and the unusual August in the graph below:

As Realtor.com explains:

As Realtor.com explains:

“While inventory continues to be in short supply, August witnessed an unusual uptick in newly listed homes compared to July, hopefully signaling a return in seller activity heading toward the fall season . . .”

While this is only one month of data, it’s unusual enough to note. It’s still too early to say for sure if this trend will continue, but it’s something you’ll want to stay ahead of if it does.

What This Means for You

If you are putting off selling your house, now may be the sweet spot to make your move. That’s because, if this trend continues, you’ll have more competition the longer you wait. And if your neighbor puts their house up for sale too, it means you may have to share buyers’ attention with that other homeowner. If you sell now, you can beat your neighbors to the punch.

But, even with more homes coming onto the market, the market is still well below normal supply levels. And, that inventory deficit isn’t going to be reversed overnight. The graph below helps put this into context, so you can see the opportunity you still have now:

Bottom Line

Even though inventory is still low, you don’t want to wait for more competition to pop up in your neighborhood. You still have an incredible opportunity if you sell your house today. Let’s connect to explore the benefits of selling now before more homes come to the market.

Why Aren’t Home Prices Crashing?

A lot of people expected prices would crash this year thanks to low buyer demand, but that isn’t happening. Why? There aren’t enough homes for sale. If you’re thinking about moving this spring, let’s connec

Two Reasons You Should Sell Your House

Wondering if you should sell your house this year? As you make your decision, think about what’s motivating you to consider moving. A recent survey from realtor.com asked why homeowners are thinking about selling their houses this year. Here are the top two reasons

How Changing Mortgage Rates Can Affect You

The 30-year fixed mortgage rate has been bouncing between 6% and 7% this year. If you’ve been on the fence about whether to buy a home or not, it’s helpful to know exactly how a 1%, or even a 0.5%, mortgage rate shift affects your purchasing power.

What Past Recessions Tell Us About the Housing Market

It doesn’t matter if you’re someone who closely follows the economy or not, chances are you’ve heard whispers of an upcoming recession. Economic conditions are determined by a broad range of factors, so rather than explaining them each in depth, let’s lean on the experts and what history tells us to see what could lie ahead. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Two-in-three economists are forecasting a recession in 2023 . . .”

As talk about a potential recession grows, you may be wondering what a recession could mean for the housing market. Here’s a look at the historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession could mean for the housing market today.

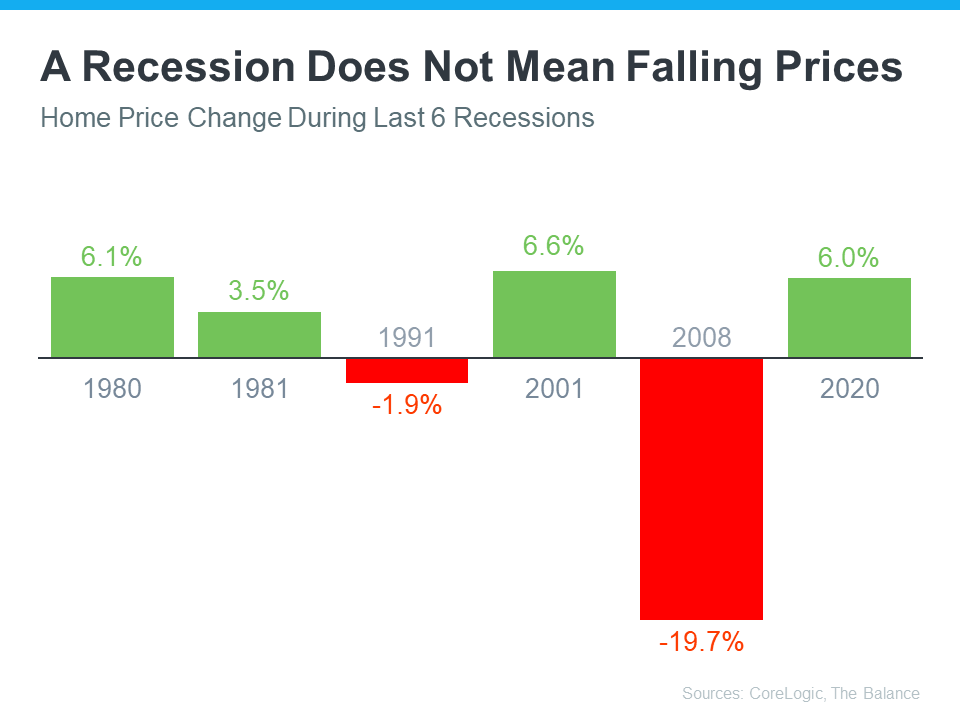

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at recessions going all the way back to 1980, home prices appreciated in four of the last six of them. So historically, when the economy slows down, it doesn’t mean home values will always fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would be a repeat of what happened to housing then. But today’s housing market isn’t about to crash because the fundamentals of the market are different than they were in 2008. According to experts, home prices will vary by market and may go up or down depending on the local area. But the average of their 2023 forecasts shows prices will net neutral nationwide, not fall drastically like they did in 2008.

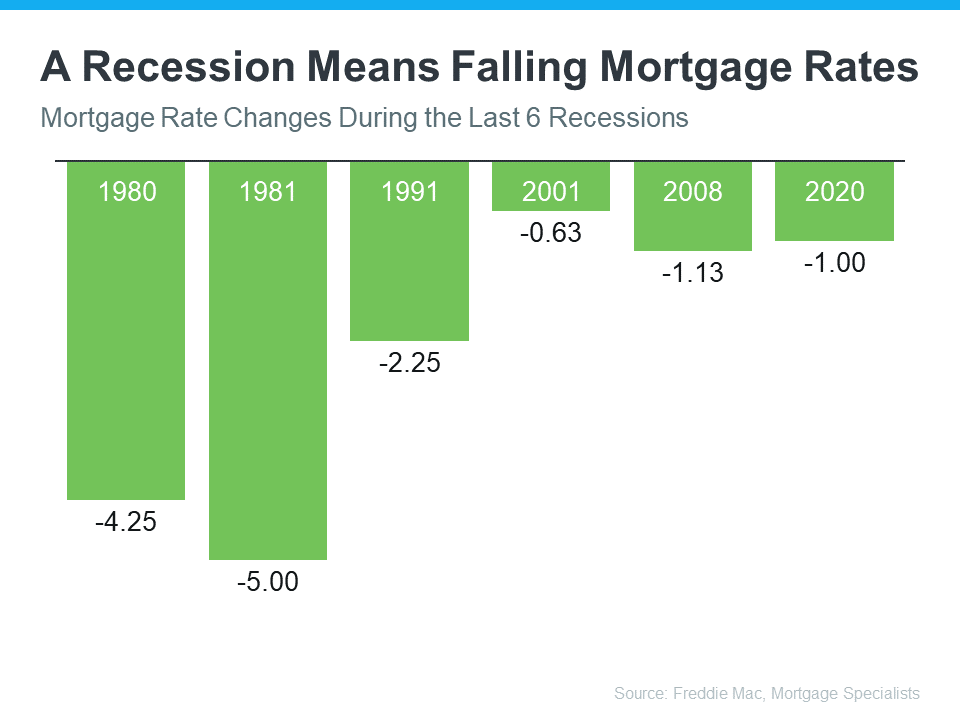

A Recession Means Falling Mortgage Rates

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the graph below shows, historically, each time the economy slowed down, mortgage rates decreased.

Fortune explains mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

In 2023, market experts say mortgage rates will likely stabilize below the peak we saw last year. That’s because mortgage rates tend to respond to inflation. And early signs show inflation is starting to cool. If inflation continues to ease, rates may fall a bit more, but the days of 3% are likely behind us.

The big takeaway is you don’t need to fear the word recession when it comes to housing. In fact, experts say a recession would be mild and housing would play a key role in a quick economic rebound. As the 2022 CEO Outlook from KPMG, says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . .

More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

Bottom Line

While history doesn’t always repeat itself, we can learn from the past. According to historical data, in most recessions, home values have appreciated and mortgage rates have declined.

If you’re thinking about buying or selling a home this year, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.

Is It Time To Sell Your Second Home?

Rear view of senior couple standing in garden of their home

During the pandemic, second homes became popular because of the rise in work-from-home flexibility. That’s because owning a second home, especially in the luxury market, allowed those homeowners to spend more time in their favorite places or with different home features. Keep in mind, a luxury home isn’t only defined by price. In a recent article, Investopedia shares additional factors that push a home into this category: location, such as a home on the water or in a desirable city, and features, the things that make the home itself feel luxurious.

A recent report from the Institute for Luxury Home Marketing (ILHM) explains just how much remote work impacted the demand for second and luxury homes:

“The unprecedented ten-fold increase towards remote work since the pandemic is an historic development that will continue to fuel second home demand for many years to come.”

But what if you bought a second home that you no longer use? If you’re now shifting back into the office or are seeing your priorities and needs change, you may find you’re not utilizing your second home as much. If so, it may be time to sell it.

And if you own what’s considered a luxury home, buyer demand for it may be even greater. In another report, the Institute for Luxury Home Marketing explains:

“. . . the last few years have left their legacy for the luxury market. While it might only represent a small percentage of the overall real estate market, luxury homeownership’s influence is growing. Not only has the purchase of homes valued over $1 million (a figure considered by the National Association of Realtors to be a benchmark for luxury) tripled from 2.6% to 6.5% since 2018, but demand for multiple luxury properties has soared over the last two years.

This phenomenal increase has been driven by a growing affluent demographic who consider owning a luxury property a necessity in their asset portfolio. All indications are that this trend is here to stay, albeit that demand is set to return to a more sustainable level.”

If you own a luxury second home that isn’t being used as much anymore, now’s the time to sell. There are still buyers in the market who are looking for a home like yours today.

Bottom Line

Let’s connect to explore the benefits of selling your second home this year.